What Is a Cash Bonus Offer? Your 2026 Guide

- The Rebel Marketer

- Jun 24

- 8 min read

A cash bonus offer is a promotional incentive that pays you extra money for completing specific qualifying actions, such as opening a new bank account, meeting a spending threshold, or referring a friend. The term “bonus” is defined as money given on top of regular pay or expected compensation. Cash bonus offers appear across banking, credit cards, and employment, and nearly all of them come with conditions you must meet to collect. Understanding those conditions is the difference between earning real money and missing out entirely.

What is a cash bonus offer, and how does it work?

A cash bonus offer is a structured financial reward tied to a specific behavior the issuer wants to encourage. Banks use them to attract new checking or savings account holders. Credit card companies use them to drive spending in the first few months after account opening. Employers use them to retain staff or reward performance. The reward is always conditional, never automatic.

The mechanics are straightforward. You complete a required action within a defined window, the issuer verifies your compliance, and the bonus posts to your account. The window matters. Most bank promotions require you to complete qualifying activity within 60 to 90 days of account opening. Miss the deadline and the bonus disappears, regardless of how close you came.

Cash bonus offers are a legitimate marketing tool. Banks treat bonuses as customer acquisition investments, expecting to recoup the cost through long-term account activity and fees. That framing matters for you as a consumer. You are not receiving a gift. You are completing a transaction with defined terms on both sides.

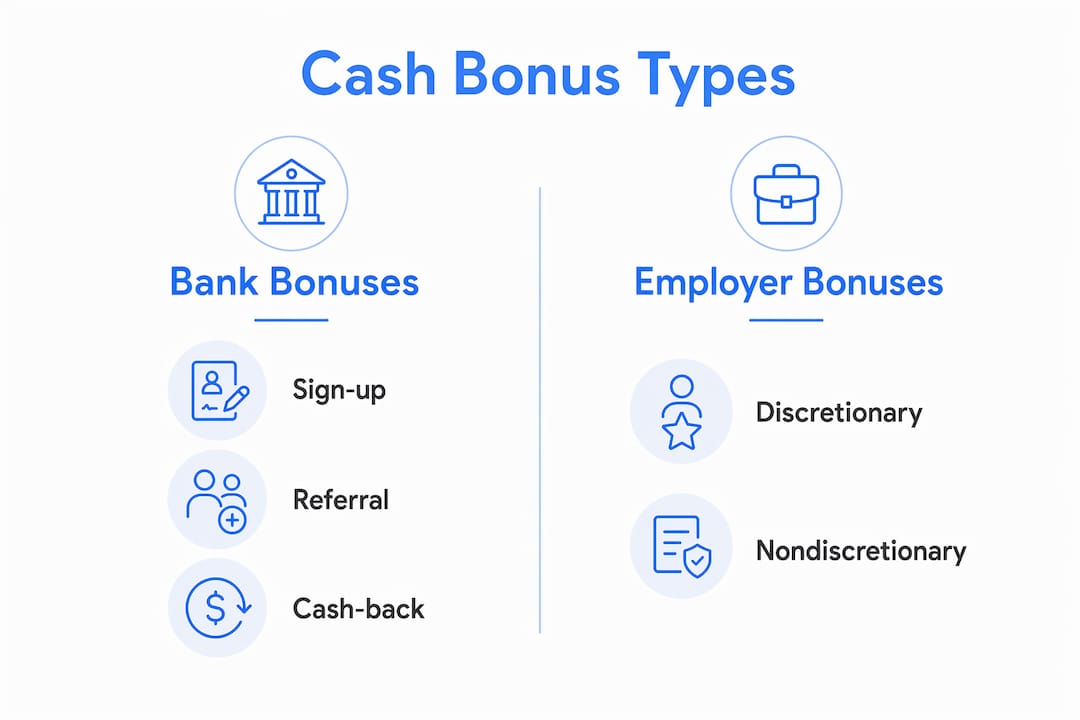

What are the main types of cash bonuses?

Cash bonuses fall into several distinct categories, each with different requirements and typical payout amounts.

Bank account sign-up bonuses

Typical bank checking account bonuses range from $100 to $500 for opening a new account and meeting qualifying deposit activity. The most common requirement is a direct deposit of a set dollar amount within the first 60 to 90 days. Some banks also require a minimum number of debit card transactions or a minimum average balance.

Credit card sign-up bonuses

Credit card sign-up bonuses require you to spend a set dollar amount within the first few months after account opening. The reward may come as a statement credit, cash deposited to a linked account, or points redeemable for cash. The spending threshold varies by issuer and card tier.

Employer cash bonuses

Employer bonuses come in two legal forms. Discretionary bonuses depend entirely on employer decisions and are not guaranteed. Nondiscretionary bonuses are contractually promised and legally owed when the employee meets the stated conditions. Performance bonuses, signing bonuses, and retention bonuses all fall into one of these two categories.

Referral and cash-back bonuses

Referral bonuses pay you when someone you recruit opens an account or completes a qualifying action using your referral link. Cash-back bonuses return a percentage of your spending as cash. Both types are common in banking, fintech, and Web3 platforms.

The table below compares the four main types at a glance.

Bonus type | Typical requirement | Typical payout |

Bank account sign-up | Direct deposit within 60–90 days | $100–$500 |

Credit card sign-up | Spend threshold in first few months | $150–$750 |

Employer bonus | Performance or contract terms met | Varies widely |

Referral bonus | Referred person completes qualifying action | $25–$200 per referral |

How do you qualify for cash bonus offers?

Qualifying for a cash incentive program requires more than just opening an account. Eligibility for bank bonuses is conditional on meeting specific requirements, so reading the terms carefully before you apply is non-negotiable.

The most common qualification steps are:

Open a new account within the promotional window. Most offers exclude existing customers or those who have held an account within the past 12 to 24 months.

Complete the primary qualifying action, such as setting up direct deposit, reaching a spending threshold, or maintaining a minimum balance.

Meet secondary requirements, which may include a minimum number of debit card transactions or keeping the account open for a defined holding period.

Wait for the posting period. Bonuses typically post within 60 to 180 days after you meet all conditions. Do not close the account before the bonus posts.

Maintain the account through the clawback window. Clawback rules allow banks to reclaim bonuses if you close the account early or fail to maintain required balances. Holding periods commonly run 60 to 180 days after the bonus posts.

Pro Tip: Take a screenshot of the full bonus terms on the day you apply. Banks occasionally update promotional pages, and having a dated record protects you if a dispute arises over whether you met the original conditions.

Documenting bonus terms at application time is one of the most practical steps you can take. Keeping screenshots or written records protects against retrospective term changes and technical interpretations that could cost you the bonus.

How are cash bonuses taxed?

Cash bonuses are taxable income. This is one of the most misunderstood aspects of cash rewards, and it affects the real value of every offer you pursue.

For employer bonuses, federal withholding runs around 22% for bonuses up to $1 million. Employers apply either the flat percentage method or the aggregate method, which adds the bonus to your regular paycheck and withholds at your standard rate. Either way, you will see a tax reduction before the money reaches your account.

Bank and credit card bonuses work differently. The bank typically issues a 1099-INT or 1099-MISC form at year end. You are responsible for reporting that income even if the bank does not send a form for smaller amounts. The IRS treats these bonuses as ordinary income, taxed at your marginal rate.

Key tax considerations for cash bonus offers:

Employer bonuses: Taxes withheld automatically at source, either at 22% flat or aggregate rate.

Bank account bonuses: Reported on 1099 forms; you pay taxes at your marginal income tax rate.

Credit card cash-back: Generally not taxable because the IRS treats it as a rebate on spending, not income.

Referral bonuses: Taxable as ordinary income; the issuer may or may not send a 1099 depending on the amount.

Cash bonuses are often misunderstood as free money without tax consequences. A $300 bank bonus may net you $210 after federal and state taxes. Factor that into your decision before you commit to meeting the requirements.

Common pitfalls when chasing cash bonus offers

The biggest mistake people make is meeting the primary requirement and assuming the work is done. Meeting the primary bonus requirement alone is often insufficient. Maintaining good account standing after the bonus posts is what prevents clawbacks.

Watch out for these specific risks:

Closing the account too early. Many banks require the account to remain open for 90 to 180 days after the bonus posts. Closing before that window triggers an automatic clawback.

Failing to maintain minimum balances. Some offers require you to keep a set balance throughout the holding period, not just at the time of the qualifying deposit.

Missing secondary requirements. Debit card transaction minimums, bill pay requirements, and mobile deposit conditions are easy to overlook and can void the bonus.

Ignoring monthly fees. A $200 bonus on an account with a $15 monthly fee that you hold for 12 months costs you $180 in fees. The net gain is $20, not $200.

Chasing bonuses that don’t fit your habits. If you don’t use direct deposit, a bonus requiring direct deposit will be difficult to earn without changing your banking behavior.

Pro Tip: Build a simple spreadsheet tracking each bonus offer, its requirements, deadlines, and the date the bonus posted. This takes five minutes to set up and prevents costly oversights.

Evaluating the math behind a bonus versus the effort and potential fees is the clearest way to decide whether a cash bonus offer is worth pursuing. If the numbers don’t work for your situation, pass on it.

Key Takeaways

A cash bonus offer pays real money only when you meet every condition, account for taxes, and avoid clawbacks throughout the holding period.

Point | Details |

Cash bonus definition | Extra money paid for completing specific qualifying actions, not a gift. |

Types of cash bonuses | Bank, credit card, employer, and referral bonuses each have distinct requirements. |

Qualification steps | Open a new account, meet the primary action, and maintain the account through the holding period. |

Tax impact | Bank and employer bonuses are taxable income; factor in your marginal rate before pursuing an offer. |

Clawback risk | Closing an account early or missing secondary requirements can trigger full bonus reclaim by the issuer. |

My honest take on cash bonus offers

Banks pay acquisition bonuses because the math works in their favor over time. That is not a reason to avoid bonuses. It is a reason to be clear-eyed about what you are agreeing to.

The offers I find most worth pursuing are ones where the required behavior matches what I would do anyway. If I already use direct deposit and keep a $500 balance, a bank bonus requiring exactly those things costs me nothing extra. The $200 or $300 bonus is pure gain, minus taxes. That is a solid return for filling out an application.

Where I see people go wrong is in chasing bonuses that require them to change their financial habits significantly. Opening a second checking account to route a fake direct deposit, or spending $3,000 in three months on a card you don’t need, creates complexity and risk. The bonus rarely justifies the behavior change.

Read the fine print on day one. Screenshot it. Set calendar reminders for every deadline. And always calculate the after-tax value before you commit. A $500 bonus sounds great until you realize it nets $340 after taxes and costs you $120 in fees over the holding period. The real gain is $220. That may still be worth it. But you should know the number before you start.

— Jacques-Louis

Curated bonus offers worth your time

Tracking down verified cash bonus offers and referral codes takes time. Jlkreiss makes that easier by curating active referral programs and bonus codes across banking, fintech, and Web3 platforms, all in one place.

The Jlkreiss Telegram channel at t.me/best_referral_codes publishes updated referral codes and bonus offers regularly, so you always have access to current deals. For a full catalog of vetted bonus programs and referral links, visit Jlkreiss and find the offer that fits your financial habits today.

FAQ

What is a cash bonus offer in simple terms?

A cash bonus offer is extra money paid to you for completing a specific action, such as opening a bank account or meeting a spending threshold. The bonus is always conditional on meeting defined requirements within a set time frame.

Are cash bonuses considered taxable income?

Yes. Bank account bonuses and employer bonuses are taxable as ordinary income by the IRS. Credit card cash-back rewards are generally not taxable because the IRS treats them as a rebate on purchases.

What is a clawback in a cash bonus offer?

A clawback is when the bank or issuer takes back a bonus you already received. It happens when you close the account early, fail to maintain a required balance, or miss a secondary condition during the holding period.

How long does it take to receive a cash bonus?

Most bank bonuses post within 60 to 180 days after you meet all qualifying conditions. Credit card sign-up bonuses typically appear within one to two billing cycles after you hit the spending threshold.

What is the difference between a discretionary and nondiscretionary bonus?

A discretionary bonus is not guaranteed and depends on the employer’s decision. A nondiscretionary bonus is contractually promised and legally owed when the employee meets the stated terms.

Recommended

Comments